Guaranty Bank Partners with Greenlight to Help Parents Raise Financially Smart Kids and Teens

Guaranty Bank is now partnering with Greenlight® Financial Technology, Inc. (“Greenlight”) to better serve families and help the next generation build healthy financial futures. Guaranty Bank customers will have free† access to Greenlight’s award-winning family finance app, available through the Greenlight for Banks program.

Research shows that 91% of kids and teens believe they need financial knowledge and skills to achieve their life goals, and 94% of parents agree.* Still, only 35 states require a personal finance course for students, and teens score an average of 64% on the National Financial Literacy Test, showing a clear gap in financial education that is accessible and effective. Parents also rank personal finance as the #1 most difficult life skill to teach their children with 81% saying they wish they had more financial education tools and resources.**

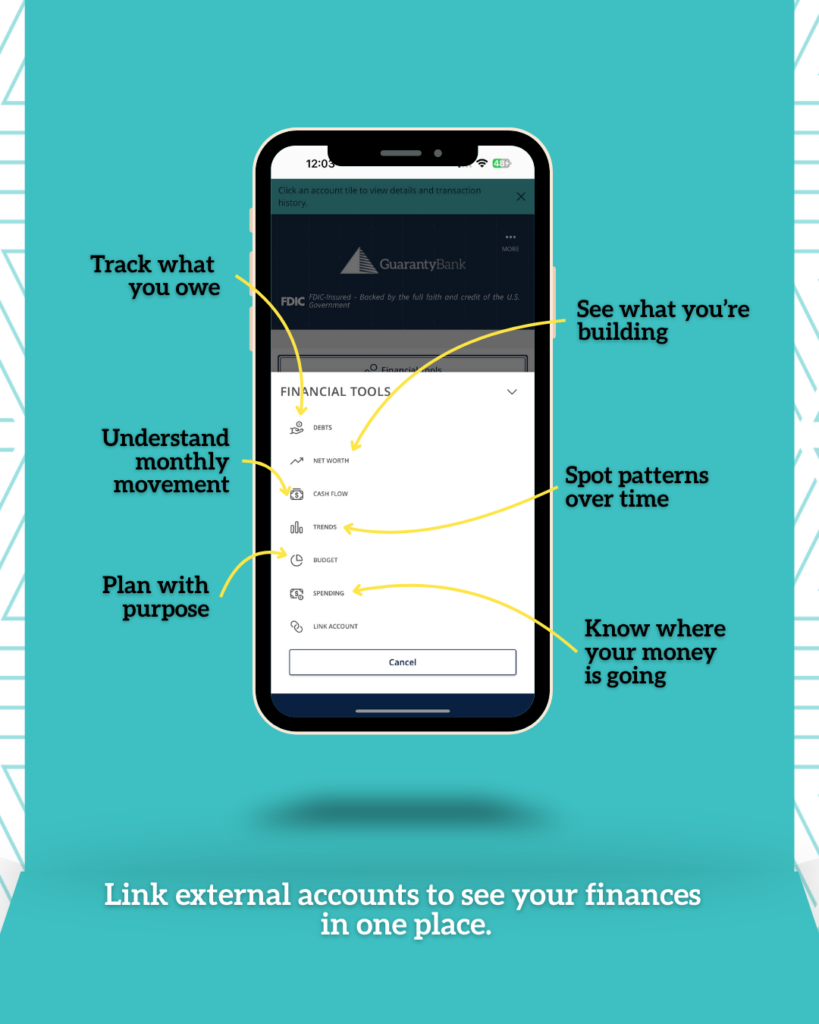

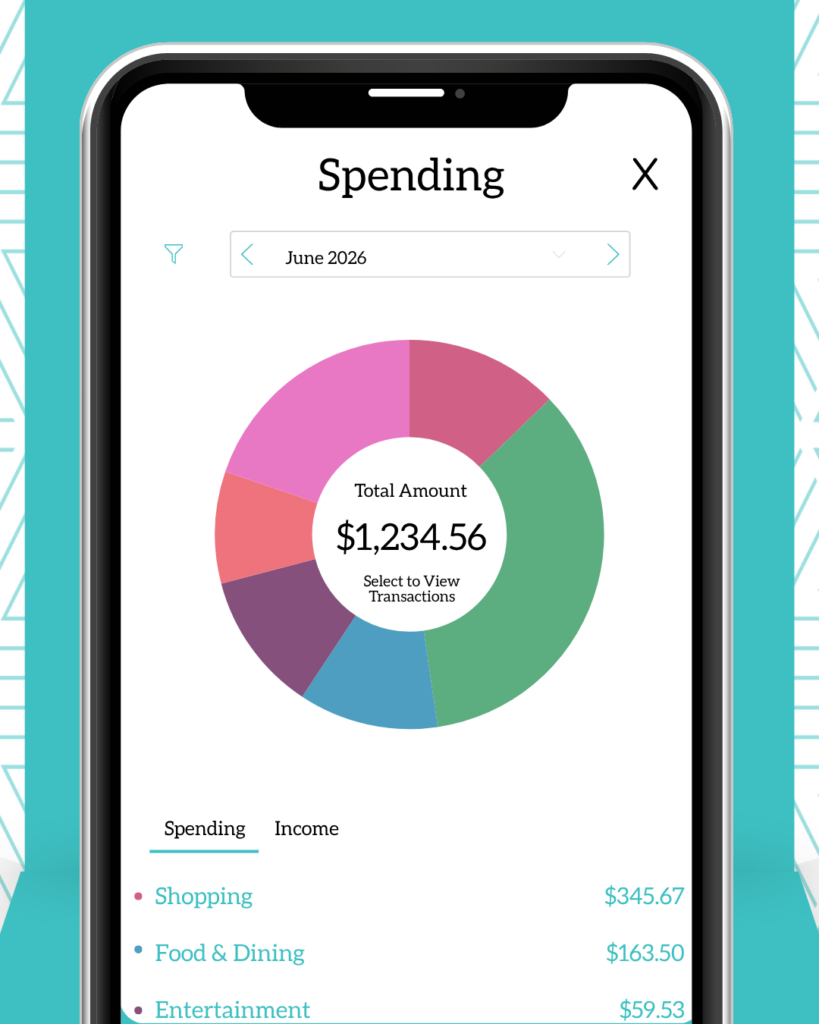

Greenlight offers a debit card and app that teaches kids and teens how to earn, save, give and spend wisely, all with parental supervision. Using the Greenlight app, parents can quickly send money, automate allowance payments, manage chores, set flexible spending controls, get real-time notifications of all transactions, and more. Kids get hands-on money management experience, along with access to Greenlight Level Up™, an in-app financial literacy game with a best-in-class curriculum, educational challenges, and rewards.

“At Guaranty Bank, we believe financial education should start early and be accessible. Our partnership with Greenlight gives parents and kids the tools they need to learn, practice, and grow together, right from their everyday banking experience,” said Hue Townsend, CEO of Guaranty Bank.

Guaranty Bank customers can receive a free† Greenlight subscription by registering through gbtonline.com/greenlight/ and adding their Guaranty Bank account as a funding source.

About Guaranty Bank:

Founded in 1943, Guaranty Bank is a privately held financial institution serving individuals, businesses, and communities across Mississippi and Tennessee. With 38 locations and a full range of consumer, commercial, mortgage, and wealth services, Guaranty Bank combines the strength of a modern financial partner with the personal relationships of a community bank. As a certified Community Development Financial Institution (CDFI), the bank is deeply committed to expanding access to financial services and supporting economic growth in the communities it serves. For more information about Guaranty Bank, please visit gbtonline.com or follow us on Facebook, LinkedIn and Instagram.

†Guaranty Bank customers are eligible for the Greenlight SELECT plan at no cost when they connect their Guaranty Bank account as the Greenlight funding source for the entirety of the promotion. Subject to minimum balance requirements and identity verification. Upgrades will result in additional fees. Upon termination of promotion, members will be responsible for associated monthly fees. See terms for details. Offer ends 6/16/2029. Offer subject to change and partner participation.

*Survey insights were collected by Greenlight through a Researchscape survey fielded between March 22 and March 24, 2024, among 2,310 respondents in the U.S., split between kids and teens ages 10-19 and parents of 10-19 year olds.

**Survey insights were collected by Greenlight through a Researchscape survey fielded between February 9-12, 2023, among 1,034 U.S. respondents, all of whom were working parents of 8-18 year olds.